Summary

Highlights

- Trump has started to impose tariffs. His approach is transactional and subject to continuous negotiations.

- We expect tariffs to be negative for growth and add inflationary pressure starting from the second half of 2025.

- We believe this will call for further diversification*, expanding the investment universe both in equities and bonds.

In this edition

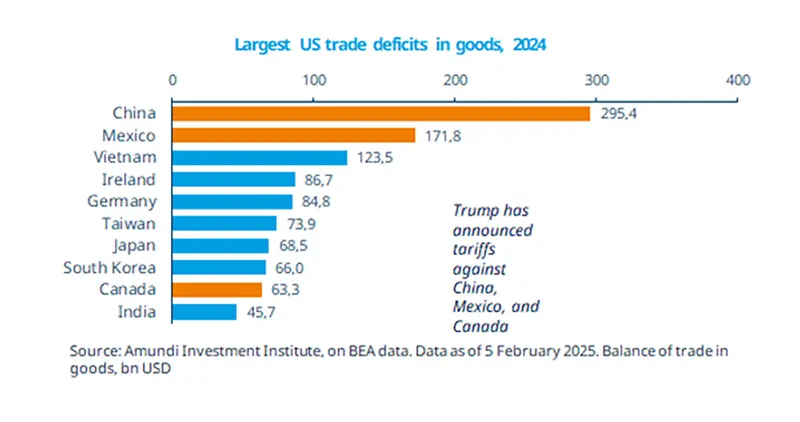

Trump’s tariff announcements have taken centre stage, with markets focusing on their impact on growth and inflation. Tariffs are primarily directed at countries with high trade deficits with the United States, starting with Mexico, Canada (currently delayed), and China. Our simulations indicate that tariffs may negatively affect economic growth and increase inflation in both the country imposing them and those affected. The size, timing, and sequence of these measures will be crucial for understanding their final impact on macro fundamentals and monetary policy responses. For this reason, we expect all players to negotiate and strive to avoid a full-blown trade war. China can implement fiscal support measures, allowing it to reallocate production chains, while Europe has less flexibility, but could accelerate reforms and investments. The situation remains fluid, with volatility dominating the markets.

Key dates

US CPI and core CPI, Fed Powell’s testimony, IND CPI

UK GDP, US PPI and core PPI

EZ GDP, US retail sales and industrial production

Read more